One of the many things on Mayor-elect Jim Strickland’s desk when he takes the oath of office on New Year’s Day is the Blueprint for Prosperity. As part of that process to develop ways to reduce poverty in Memphis 10 points in 10 years, 15 experts at University of Memphis wrote issues briefs in key areas such as health, economics, education, human services, business development, energy reduction, housing and community development, and transportation. Dr. David Cox managed the process and contributed significantly to the project

In the coming weeks, we’ll post some of these issues briefs, which have not been published previously, because they contain important insights into addressing poverty in Memphis. Each of the briefs provide a context for issues and recommendations for attacking poverty, such as those in this issues brief, including Memphis increasing the minimum wage and the numbers of people receiving the Earned Income Tax Credit.

We’re starting today with human services, case management, and financial counseling written by two people who are extraordinary sources of knowledge and recommendations for action, Dr. Elena Delavega and Dr. Steven Soifer in the Department of Social Work, School of Urban Affairs and Public Policy:

Executive Summary

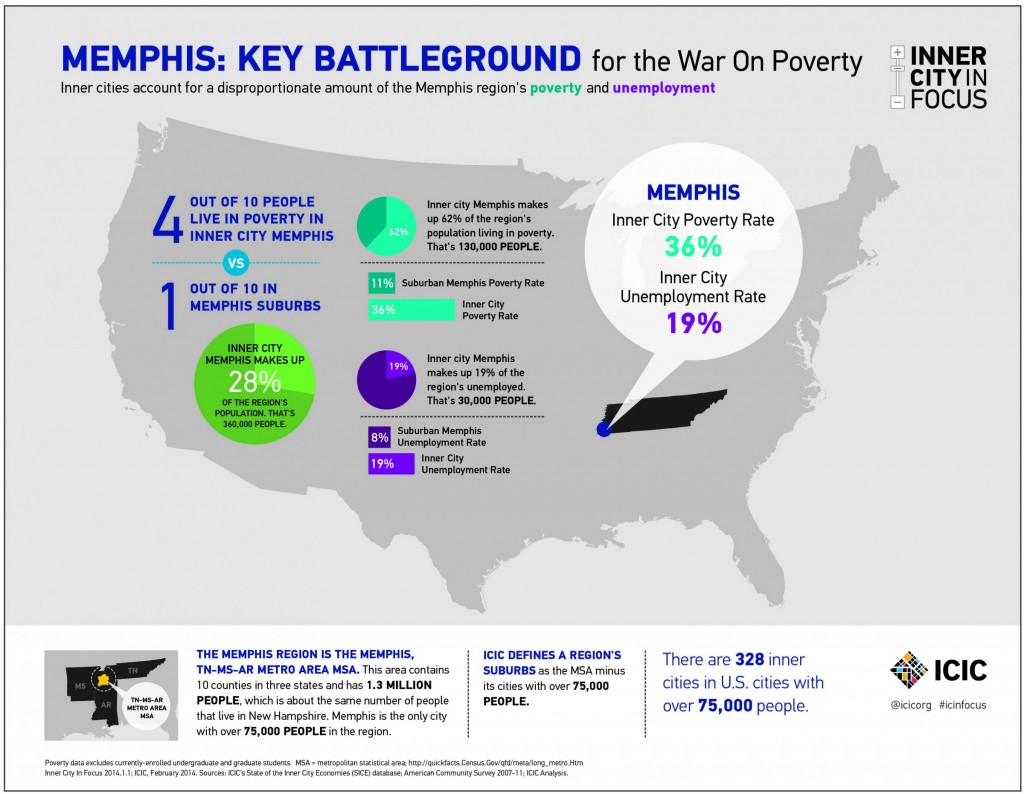

For the second year in a row, Memphis has earned the dubious honor of having the highest poverty rate for a large metropolitan area (over 1,000,000 in population). The alarming poverty rate in Memphis has a particularly deleterious impact on families, with almost half of our children living in poverty (Delavega, 2014a). The basic problem of poverty is inadequate resources: not having the necessary funds to pay for life’s necessities. Financial capability has been defined as “making ends meet and keeping track “(Atkinson, McKay, Kempson, & Collard, 2006). Simply put, poverty means lacking the income; income management is foundational elements in escaping poverty. The city of Memphis can help working families escape poverty through promoting full employment at adequate wages, full participation in the Earned Income Tax Credit (EITC), and access to financial literacy and mainstream banking services.

Introduction

This paper directly addresses the way in which the city of Memphis can promote increased income acquisition and management (financial capacity) among low‐income families: Employment and wages, the Earned Income Tax Credit (EITC), and financial literacy and access to banking.

In this paper, the authors make five recommendations to strengthen the financial capacity of Memphians:

Recommendations to Increase Income.

* Full Employment. Promote full employment through tax credits and utilizing the local government as the employer of last resort.

* Adequate Wages. Implement a city ordinance increasing the minimum wage to $12 an hour.

* The Earned Income Tax Credit (EITC). Create partnerships with local employers and agencies to increase the participation of low‐income residents in the EITC.

Recommendations to Promote Financial Capacity.

* Financial Literacy. Partner with local agencies and banks to provide financial literacy training at the most basic levels for low‐income Memphians.

* Banking Access. Partner with local banks to increase access to mainstream banks and banking services for low‐income residents and the unbanked.

The authors of this brief paper first define the issues and address the existing barriers to solving these issues; secondly, we provide solutions that the city of Memphis can implement to immediately address each locally.

Section 1: Low Income and Lack of Financial Capacity

Employment and wages have a direct impact on poverty rates. Without employment at adequate wages, people do not have access to the most basic financial resources without governmental assistance.

Section 1a: Employment. Memphians’ participation in the labor force remains weak after the financial crisis of 2008. Memphis has had a particularly slow recovery and still suffers an unemployment rate of 9.2%, much higher than the national average of around 5% (Delavega, 2014b). Given the social costs of unemployment (i.e., crime, poverty) (Burtl, 2010; Wheelock, Uggen, & Hlavka, 2011), promoting full employment will lead to shared prosperity in Memphis.

According to the U.S. Department of Health and Human Services (2015) a family of four needs $24,250 a year to be above poverty. However a full‐time worker making the minimum wage only earns $15,080 a year. It is not surprising that over 27% of Memphians live under poverty; given that in Memphis 22% of the households have earnings below $15,000, an income far below poverty.

Section 1c: Failure to Claim the Earned Income Tax Credit

In Memphis, 20% of the lowest‐income households in the poorest neighborhoods are not claiming the Earned Income Tax Credit (EITC), a refundable tax credit American citizens or permanent residents can receive if they have earned any income in a fiscal year. Among neighborhoods with poverty rates greater than 40%, the non‐claim rate is greater than 30%. The Vance Avenue area has a non‐claim rate of 67% among those earning less than $10,000 (Delavega, 2014c).

Very conservative estimates suggest that the city of Memphis (Delavega, 2014c) potentially loses anywhere from $30,000,000 to $70,000,000. The money lost to Memphis in unclaimed EITC would be an important contribution to our local prosperity. When wehave up to seventy million dollars possibly lost to Memphis; it is easy to imagine that could do a lot with that money.

Section 1d: Lack of Financial Capability

As defined here is capacity to function well in financial matters both from the existence of resources standpoint, and from the optimal management of said resources standpoint (Leskinen & Raijas, 2006). Essentially, it means having the resources to meet financial responsibilities (i.e., living expenses) and the knowledge to manage said resources effectively and efficiently over the long term (Atkinson et al., 2006). If Memphians do not have the means to manage efficiently and competently the resources they do have, these resources are very likely to be squandered and mismanaged. It is important then to insure people have the knowledge of how to protect their resources and have resources to protect. There is an enormous body of research documenting the positive impacts of financial literacy (Sherraden, Johnson, Guo, & Elliott; 2011), particularly in promoting increased income. Promoting living wages, the Earned Income Tax Credit, affordable interest rates, and access to banking as well as financial education will work together to increase the financial capability of our region.

Section 1e: The Unbanked

According to the Corporation for Enterprise Development (CFED), Memphis is the 5th most unbanked city in the U.S. with more than 100,000 households in this category (CFED, 2009). While nationally 7.7 percent of the population is “unbanked” (have no bank accounts) and 17.9 percent are “underbanked” (have an account, but rely on high interest alternative financial services), in Memphis the numbers are 16.7 percent and 28.1 percent respectively. Shelby County is also the 7th most unbanked county with populations over 100,000 in the U.S., with 14 percent unbanked and 25.8 percent underbanked (data from 2009).

The Federal Reserve Bank of St. Louis states the “the most common groups of unbanked persons include those who are less‐educated, households headed by women, young adults and immigrants.” (Beard, 2010). Fees can range from 2.5 to 5 percent for check cashing services on government and payroll checks. (Beard, 2010), which creates high costs for those who can least afford them.

Part of the problem is that the state of Tennessee “has one of the highest concentrations of payday lenders per capita” (Cox, 2015). Thus, according to the Bank On Memphis (2015), people making about $20,000 per year can end up spending about 6 percent or $1200 in fees each year that they can ill afford. Moreover, in states like Tennessee, title loan companies are to be found on almost every street and corner in low‐income neighborhoods. People often get only about 25% of the value of their car as a loan, which carries exorbitant interest rates on it (Cox, 2015).

Section 2: Proposed Local Solutions

In this section, we explore the actions that the city of Memphis can take to address issues of employment and wages, failure to claim the Earned Income Tax Credit, and financial management and stewardship through banking the unbanked.

2a: Promote full employment. Unemployment, of course, is a big barrier to earnings. The city of Memphis shouldbecome the employer of last resort. It costs over 4$0,000 a year to incarcerate a person. Offering employment opportunities would prevent crime, incarceration, and would be more economical than incarceration. The city can hire workers to rebuild the infrastructure of the city and to provide maintenance such as park cleanup or street sweeping. In addition to hiring workers, the city can provide tax incentives to companies that employ large numbers of low‐skill workers or people with criminal records. The tax benefits, reduction in incarceration costs, and multiplier effects on the local economy would more than make up for the tax breaks provided to employers.

2b: Enact a city ordinance increasing minimum wages to $12 an hour. Employment, of course, is not enough without adequate wages. Increasing the minimum wage to $12 an hour would be sufficient to bring a family of four of out of poverty. A wage of $12 an hour for a year‐round, full‐time worker represents earning of $24, 960, above the poverty threshold for a family of four in 2015. This action by the city of Memphis would help the 38% of Memphis households with incomes below the federal povertythreshold and would reduce the poverty rate significantly when used in conjunction with increased employment opportunities for all Memphians.

Section 2c: Promote full‐participation in the EITC through local partnerships. Create partnerships with local employers and agencies to increase the participation of low‐income residents in the EITC. From January to May 2015, the Department of Social Work at the University of Memphis had 48 students trained to provide Volunteer Income Tax Assistance (VITA) to low‐income Memphians. This service can be increased by engaging agencies and local businesses. The Department of Social Work can serve as a training partner, and the local agencies and businesses can provide volunteers and spaces to assist Memphis’ families with incomes below $50,000. If the city maximizes every federal penny owed to Memphis, the economic impact on the city can be as great as $350,000,000 due o multiplicative effects.

Section 2d: Financial Literacy. Partner with local agencies and banks to providefinancial literacy training at the most basic levels for low‐income Memphians. The University of Memphis can provide the curriculum and training, and local banks and agencies can provide space and volunteers, as well as assist with the sharing of information. Volunteers can help people receiving their EITC develop budgets and with savings and investments plans to leverage the EITC for the future.

2e: Increase access to mainstream banking among the unbanked. The Federal Reserve Bank is working with the city of Memphis and the RISE (Responsibility, Initiative, Solutions, Empowerment) Foundation to reduce the rate of unbanking and underbanking in the city. In addition, a number of banks and credit unions are taking part in an effort called Bank On Memphis to offer no or low‐fee accounts to low‐ income customers). The goal is a modest 5‐7,000 new household accounts. Similar efforts in San Francisco have led to the banking of 50,000 new people (http://www.memphisdailynews.com/editorial/ArticleEmail.aspx?id=51547).

Unfortunately, the program has gotten off to a slow start, leading Mayor Wharton of Memphis to restart the initiative in late 2012 (http://www.memphisdailynews.com/news/2013/feb/4/mayor‐banks‐revive‐program‐ targeting‐citys‐unbanked/). Expanding access to mainstream banking services willallow low‐income Memphians to avoid high‐cost check cashing and payday loan services, andwill promote budgeting and savings.

An Additional Concern: Food Deserts

According to the United States Department of Agriculture (USDA), “food deserts are defined as urban neighborhoods and rural towns without ready access to fresh, healthy, and affordable food” (2015). According to research by Ken Reardon, Professor in the City and Regional Planning Department at the University of Memphis (UofM), “only seven out of 77 census tracks in urban Memphis have access to a full‐service supermarket,” while neighborhood grocery stores and fast food outlets are common, but more expensiveand offer less healthy food options (http://www.memphisdailynews.com/news/2013/jul/8/food‐desert‐oasis/).

Memphis is considered America’s fourth worse urban food desert. Moreover, the city is considered #1 in the country for hunger, since ¼ of the population reported not being able to feed its family sometime during 2010. Finally, over 80 percent had to choose at some point to buy food rather than paying their utility bill, and almost 1/3 had to make the choice of food or rent/mortgage at some point in 2010 as well (NewsOne, 2011).

One solution to this problem is “the Green Machine,” a joint effort of St. Patrick’s church, VAC (the Vance Avenue Collaborative), and the City and Regional Planning Dept. at UofM. This bus offers a “mobile food market” that offers fresh and healthy produce at reasonable prices in 15 different parts of Memphis. Another solution was the opening of the South Memphis Farmers Market in 2010, organized by city residents, The Works, a local community development corporation, and the UofM (http://www.memphisdailynews.com/news/2013/jul/8/food‐desert‐oasis/). Other solutions might include Seattle’s “pop‐up” grocery stores (not unlike Memphis’s Green Machine), or New Orleans and other cities experiments in urban farming (Business Insider, 2015).

Conclusion

Increasing income through employment, adequate wages, and full participation in the EITC will contribute very directly to the elimination of poverty. However, without the capacity to adequately manage household finances, increased resources may be squandered. It is thus important to increase the financial literacy of Memphians and access tomainstream banking services. The solutions presented here will increase the financial capacity of our

city in two main ways: Increased resources, and improved resource management. The solutions proposed here can be immediately and directly implemented by the city without waiting for the state or federal governments to act.

Citations:

Atkinson, A., McKay, S., Kempson, E., & Collard, S. (2006). Levels of financial capability in the U.K.: Results of a baseline survey. Financial Services Authority, University of Bristol. Retrieved from http://www.esds.ac.uk/doc/5697%5Cmrdoc%5Cpdf%5C5697results.pdf

Bank On Memphis. (2015). Why bank? Retrieved from http://www.bankonmemphis.org/bank‐account‐savings.html

Beard, M. P. (2010). In‐depth: Reaching the unbanked and underbanked. Central Bank: A Publication of the The Federal Reserve Bank of St. Louis. Retrieved from https://www.stlouisfed.org/Publications/Central‐Banker/Winter‐2010/Reaching‐the‐ Unbanked‐and‐Underbanked

Burtl, R. M. (2010). More than a second chance: An alternative employment approach to reduce recidivism among criminal ex‐offenders. Tennessee Journal of Law and Policy 6(1), 9‐45.

Business Insider. (2015). 10 American food deserts where it is impossible to eat healthily. http://newsone.com/1540235/americas‐worst‐9‐urban‐food‐deserts/

Cox, N. (2015). Unbanked and overcharged. Memphis OTL. Retrievedfrom http://www.memphisotl.com/living/unbanked‐and‐over‐charged/

Corporation for Enterprise Development [CFED]. (2009). The most unbanked places in America. Retrieved from http://cfed.org/assets/pdfs/Most_Unbanked_Places_in_America.pdf

Delavega, E. (2014a). 2014 Memphis poverty [Fact Sheet]. University of Memphis’ Department of Social Work. Retrieved from http://www.memphttp://www.bankonmemphis.org/bank‐account‐ savings.htmlhis.edu/socialwork/2014povertyfactsheet.pdf

Delavega, E. (2014b). 2014 Memphis unemployment [Fact Sheet]. University of Memphis’ Department of Social Work. Retrieved from http://www.memphis.edu/socialwork/2014memphisunemployment.pdf

Delavega, E. (2014c). The missing piece in Memphis’ economy. [EITC Fact Sheet]. University of Memphis’ Department of Social Work. Retrieved from https://www.memphis.edu/socialwork/pdfs/Non‐ Claim%20Rates%20in%202011%20Released%20in%202014.pdf

Leskinen, J., & Raijas, A. (2006). Consumer financial capability – a life cycle approach (pp.8‐ 23). In The European Credit Research Institute’s Consumer Financial Capability

***

Join us at the Smart City Memphis Facebook page for daily articles, reports, and commentaries that are relevant to Memphis.

If bringing a family of four out of poverty by enacting a $12/hr minimum wage will help the situation why not just enact a $30/hr minimum wage? If $12/hr equates to $24,960/yr then $15 equates to $62,400, surely that accomplishes stated goal even better. If everyone in the metro area were suddenly making 60k plus through legislation think about how great the local economy would be. New car sales would be through the roof, new home construction would be booming, etc.